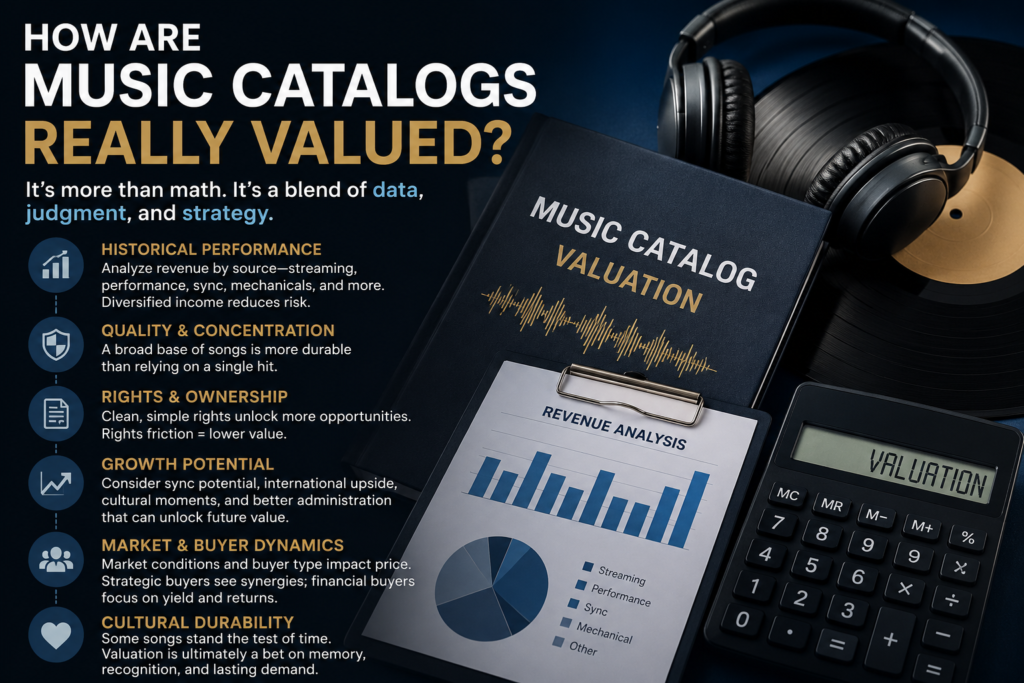

Music catalog valuation looks simple from the outside. A buyer studies the royalty statements, decides what the songs have earned, puts a multiple on that income, and arrives at a price. In reality, it is far messier. A catalog is not a factory with fixed outputs. It is a living asset shaped by consumer taste, licensing activity, artist reputation, platform shifts, and how actively the rights are managed. That is why the best way to understand valuation is to think of it as a blend of math, judgment, and strategy.

The first layer is historical performance. Buyers want to know what the catalog has actually done, not what someone hopes it might do. That means looking closely at the last several years of revenue by source. Streaming is usually the headline number because it is visible, recurring, and easy to model. But streaming is only one part of the picture. Performance income, mechanicals, sync licensing, neighboring rights, and other revenue streams can all matter. A catalog with diversified income is often more attractive than one that depends almost entirely on a single source. Diversification lowers risk and gives the buyer more confidence that a sudden change in one channel will not break the investment thesis.

The second layer is quality of income. Not every dollar is equally valuable. If a catalog’s earnings come from a broad base of songs that continue to show up year after year, that is different from a catalog where one song carries everything. Concentration risk matters. A catalog built on one monster track can still be valuable, but the valuation process has to account for the possibility that interest in that one song fades. A deeper catalog with multiple recognizable works may look less flashy on paper but can be more durable over time.

Then there is the question of rights. Are you buying publishing, masters, or both? Do the songs have straightforward ownership, or are there samples, multiple writers, conflicting approvals, and legacy complications? Rights friction can reduce value because it slows down monetization. A film and television supervisor wants a clean path. If every placement turns into a multi-party negotiation, some opportunities disappear before they begin. In other words, two songs with similar streaming profiles can have different valuations because one is easier to exploit commercially.

Another major input is growth potential. Buyers do not pay only for what happened yesterday. They are trying to estimate what the catalog can earn tomorrow. That is where the process gets subjective. Can the catalog benefit from sync licensing? Is there international upside? Does the artist have an anniversary, documentary, biopic, or cultural reappraisal on the horizon? Could better administration or marketing unlock value that the current owner never pursued? Those questions matter because a buyer is not just buying income; they are buying the right to operate the asset better.

Still, buyers have to be careful not to overpay for upside that may never arrive. A biopic, viral rediscovery, or social media resurgence can meaningfully lift a catalog, but those events are hard to predict with confidence. You cannot build an investment case entirely on wishful thinking. That is why seasoned buyers usually separate the base case from the blue-sky case. The base case depends on what the catalog is already proving in the market. The upside case is where smart operators can outperform, but it should not be the only reason the deal works.

Market conditions matter too. In a hot market, buyers may stretch on multiples because they believe music rights are scarce, attractive, and resilient. In a colder market, underwriting gets tougher and assumptions get stricter. Investor sentiment, interest rates, and access to capital all influence what feels like a reasonable price. A catalog is not valued in a vacuum. It is valued in a competitive market where different buyers have different cost-of-capital structures and different exit expectations.

That brings up another overlooked issue: not every buyer values the same catalog the same way. A strategic music company may pay more than a financial buyer because it can integrate the rights into a broader platform. It may already have sync teams, global infrastructure, label relationships, and marketing channels that create incremental value. A private equity-style buyer, by contrast, may be more disciplined about cash yield and hold period. One sees synergies. The other sees return thresholds. Both are evaluating the same songs, but they are not solving for the same outcome.

There is also a human element. Cultural relevance is difficult to reduce to a spreadsheet. Some songs have an emotional permanence that numbers only partially capture. They keep resurfacing at weddings, in stadiums, on classic playlists, in movie trailers, and in new generations’ listening habits. Catalog investors are ultimately making a bet on memory, recognition, and recurring demand. They are asking whether people will keep caring.

So how are music catalogs really valued? By looking backward at revenue, sideways at risk, and forward at possibility. Historical cash flow sets the floor. Rights quality, concentration, licensing potential, and operational strategy shape the premium or discount. Market conditions and buyer type influence the final price. The spreadsheet matters, but so does judgment. That is why catalog valuation is never just arithmetic. It is the art of deciding how much cultural durability is worth in financial terms.