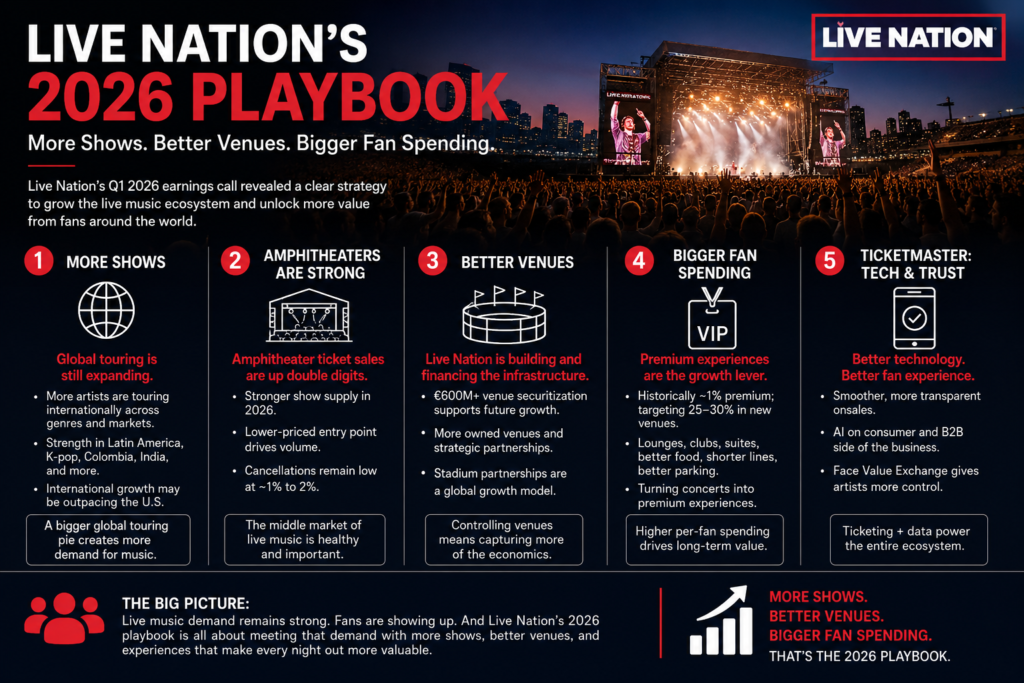

Live Nation’s first-quarter 2026 earnings call offered a clear look at where the live music business is heading.

The short version: Live Nation is not just betting on more concerts. It is betting on a bigger live music ecosystem — more global touring, more stadium and amphitheater activity, more owned and partnered venues, better ticketing technology, and higher per-fan spending through premium experiences.

For the music business, that matters. For catalog owners, labels, artists, investors, and anyone watching the economics of music, Live Nation’s call was a reminder that streaming is only one piece of the puzzle. The real money is often built around the fan relationship.

Live music is where that relationship becomes visible.

More Shows: The Global Touring Machine Keeps Expanding

One of the strongest messages from Live Nation management was that global concert supply remains healthy.

CEO Michael Rapino said more artists are touring globally, and that the live music “pie” continues to grow. He pointed to global supply from regions and genres including Latin America, K-pop, Colombia, India, and other international markets. In his view, more artists from more parts of the world are now able to tour across clubs, theaters, arenas, festivals, and stadiums.

That is an important point. Live Nation is not framing growth as dependent on one superstar tour or one geography. The company is talking about a broader, more globalized touring market.

For Catalogs and Cash, this is the key idea: music catalog value becomes more interesting when the audience becomes global.

An artist’s catalog is not just a static bundle of songs collecting streaming royalties. It can become part of a much larger commercial system. Touring can reintroduce fans to older songs. Festivals can expose legacy acts to younger audiences. International markets can create new demand for music that may have already matured in the U.S. or Europe.

The more global the fan base becomes, the more ways there are to monetize the music.

Amphitheaters Are Back in the Story

Live Nation also spent time addressing amphitheaters, which had been a concern in the prior year. Rapino said the company has stronger amphitheater supply in 2026, and that ticket sales are tracking ahead of last year by double digits. He also pushed back on concerns about cancellations, saying the company typically sees a 1% to 2% cancellation rate and that 2026 does not look unusual.

That matters because amphitheaters occupy an important middle lane in the concert business.

Not every artist is a stadium act. Not every catalog is attached to a mega-star. But there is a lot of durable value in artists who can consistently fill amphitheaters, theaters, clubs, and festivals.

Amphitheaters also have a pricing advantage. Rapino described them as a lower-cost entry point compared with arenas and stadiums. That makes them a volume business. For fans who may not want to spend stadium-level money, amphitheaters offer a more accessible live music experience.

This is where the long tail of the music business becomes interesting. Legacy rock acts, country artists, jam bands, alternative bands, nostalgia tours, and multi-act summer packages can all fit into this model.

A catalog does not need to dominate Spotify to have commercial value. Sometimes the better question is: Can this music still move people out of the house?

If the answer is yes, there may be more value there than the streaming chart suggests.

Better Venues: Live Nation Wants More Control of the Infrastructure

The second part of Live Nation’s playbook is venue strategy.

Live Nation is not just promoting shows. It is building, buying, financing, and partnering around venues. CFO Joe Berchtold discussed a venue securitization transaction of just over €600 million, using certain venues as collateral. He described the company’s venue strategy as having something like a property-company/operating-company structure, while still keeping the assets under one roof.

That may sound technical, but the business idea is simple: venues are strategic assets.

If Live Nation controls more of the venue footprint, it can capture more of the economics around the concert. That includes ticketing, sponsorship, food and beverage, premium experiences, parking, hospitality, and long-term fan data.

This is one of the most important ideas in the modern music business: the money is not only in the music itself. It is in the infrastructure around the music.

A song gets the fan interested.

The artist gets the fan emotionally committed.

The venue turns that attention into a night out.

The ticketing platform captures the transaction.

The premium experience increases the spend.

The sponsor attaches a brand to the moment.

That is the full stack of live music monetization.

Stadium Partnerships Could Become a Global Growth Model

Live Nation also discussed stadium partnerships in Argentina, including arrangements involving Club Atlético and River Plate Stadium. Rapino said the company likes partnering with stadiums globally because many of them are underused compared with NFL-style venues in the U.S.

That is a very interesting model.

Instead of always building from scratch, Live Nation can partner with existing stadiums, bring concerts into the building, add sponsorship expertise, and sometimes provide capital. This can be less capital-intensive than owning or building every venue outright, while still allowing Live Nation to lock up important revenue streams.

For the music industry, this points to a broader trend: live music is becoming more professionalized, more global, and more infrastructure-driven.

For catalog investors, this matters because a stronger live infrastructure can extend the life of music assets. If older artists, reunion tours, tribute events, anniversary shows, and festival appearances become easier to route and monetize globally, then catalogs tied to those artists may have more ways to stay culturally and commercially relevant.

Bigger Fan Spending: Premium Is the Growth Lever

The most interesting part of the call may have been Live Nation’s comments on premium fan experiences.

Rapino said concerts have historically been roughly 99% general admission or standard experience and only 1% premium. But Live Nation sees an opportunity to change that. He said some new arenas could have up to 30% of the house in a premium capacity, while amphitheaters could move from low-single-digit premium levels toward 25% premium.

That is a major shift.

Live Nation wants concerts to look more like sports venues. That means better parking, shorter lines, better food and beverage, hospitality rooms, suites, boxes, lounges, and upgraded experiences.

This makes sense. Fans are not only paying for music. They are paying for the night.

The seat matters.

The parking matters.

The line matters.

The drink matters.

The bathroom matters.

The ability to avoid chaos matters.

For younger fans, the concert may be a social-media-worthy experience. For older fans, comfort may be the reason they are willing to attend at all. A 50-year-old fan who loves a legacy artist may not want to fight lawn traffic, wait in long lines, or stand all night. But that same fan may pay more for a better experience.

That creates a huge opportunity around legacy catalogs.

Older catalogs often have older fans. Older fans often have more disposable income. If Live Nation can improve the premium experience, it can increase per-fan spending without needing every fan to be a teenager streaming songs all day.

That is a very different way to think about catalog value.

Ticketmaster Is Still Central to the Strategy

Ticketmaster also came up repeatedly on the call.

Rapino said the company is focused on making the onsale process smoother, more transparent, and more confidence-building for fans. He also mentioned using AI on both the consumer side and the B2B side, while building out tools like Face Value Exchange for artists.

Berchtold added that Ticketmaster is using newer approaches, including AI tools, to move faster in markets like Latin America, Asia, and Japan.

The strategic point is clear: ticketing is not just a transaction layer. It is part of the fan relationship.

Who controls the ticketing experience controls a valuable part of the music economy. That company sees demand, pricing, geography, artist strength, fan behavior, and purchase intent.

For artists and catalog owners, this matters because fan data is becoming one of the most important assets in music. A catalog tells you what people listen to. Ticketing tells you what people will leave the house and pay for.

Those are not the same thing.

No Demand Pullback — At Least Not Yet

Live Nation also addressed the big investor question: are consumers pulling back?

Rapino said the company is not seeing a demand slowdown across genres, demographics, geographies, venue types, or price points. He pointed to everything from club shows to amphitheaters to expensive stadium shows and said demand remains strong.

That is a powerful statement, especially in an economy where people keep looking for signs of consumer weakness.

Live music appears to remain a priority. Fans may cut back elsewhere, but the concert is still a major social event. For some fans, it may be one of the few big nights out they plan around all year.

That supports a broader thesis: music remains emotionally durable.

People may change how they consume it. They may shift from CDs to downloads to streaming to short-form video. But the desire to gather around music has not disappeared.

In some ways, it may be stronger because so much of modern life is digital. The live show is physical, social, scarce, and memorable.

That is why it commands pricing power.

The Catalogs and Cash Takeaway

Live Nation’s 2026 playbook is simple:

More shows.

Better venues.

Bigger fan spending.

But underneath that is a bigger music business lesson.

The value of music is not limited to streaming royalties. Music creates identity, memory, community, and live demand. The companies that can turn that demand into experiences, venues, sponsorships, ticketing, hospitality, and global touring routes are building around the music in ways that can be extremely valuable.

For catalog investors, this should matter.

A catalog is not just a spreadsheet of historical royalties. It is a living asset connected to fan behavior. If the artist can tour, if the music can support a festival slot, if the fan base has spending power, if the songs still create emotional pull, then the catalog may have value beyond passive streaming income.

Live Nation’s call showed that the live music economy still has momentum. The company is investing in venues, expanding globally, improving ticketing, and trying to increase per-fan monetization through premium experiences.

That is not just a concert story.

That is a music asset story.

Bottom Line

Live Nation’s Q1 2026 call was a reminder that the music business is bigger than the stream count.

Streaming tells us what people play.

Concerts tell us what people will pay for.

Venues show where the money gets captured.

Premium experiences show how much more the night can be worth.

And that is the real Catalogs and Cash lesson: the future of music value may belong to the companies that understand not only the song, but the entire economy around the fan.