By 2026, the music catalog business has become something bigger than nostalgia.

It’s infrastructure.

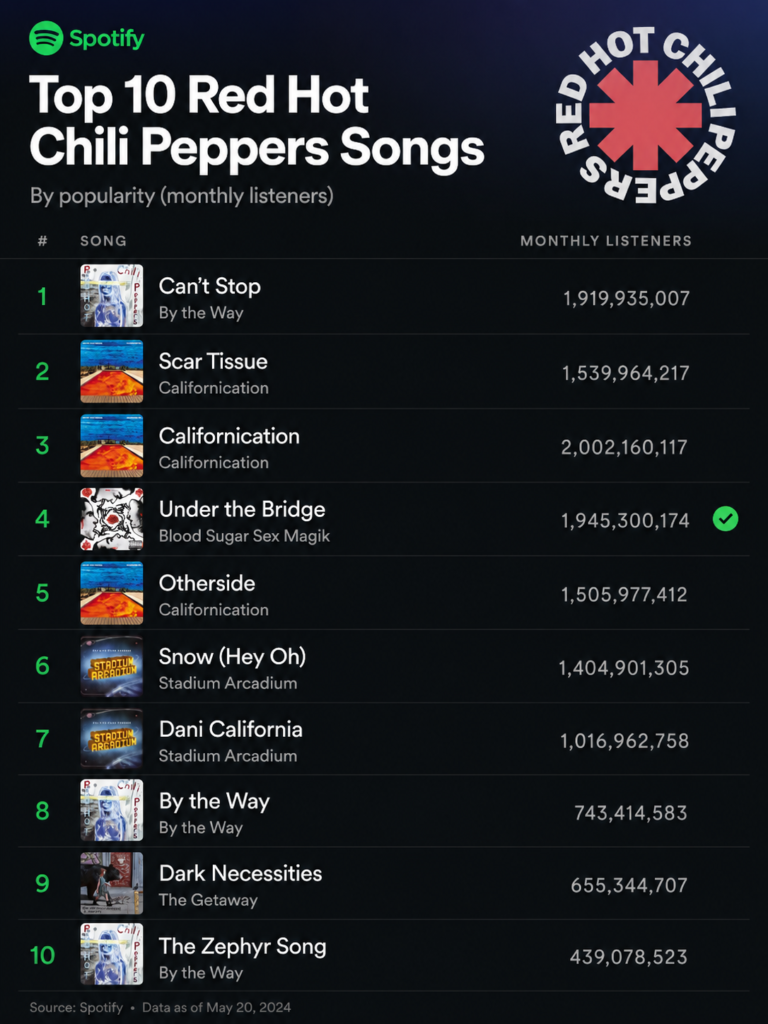

This week, the Red Hot Chili Peppers, with over 46 million monthly listeners on Spotify, reportedly sold their recorded music catalog to Warner Music Group for more than $300 million — one of the largest rock catalog deals in recent memory.

According to Rolling Stone and The Hollywood Reporter, the deal covers the band’s master recordings — the actual sound recordings behind hits like “Californication,” “Under the Bridge,” “Scar Tissue,” “Can’t Stop,” and “Otherside.” They are also the 8th most-played band on SiriusXM Lithium 90’s rock, even though their catalog spans five decades.

And here’s the key detail:

This comes after the band already sold its publishing rights years ago for roughly $140–150 million.

That means the market is now valuing two separate layers of music ownership at enormous scale:

- Publishing rights (songwriting/composition)

- Master recordings (the recordings themselves)

The Chili Peppers are essentially monetizing decades of cultural relevance twice.

Why Music Catalogs Became Wall Street Assets

Music used to be viewed as entertainment.

Now it’s increasingly viewed as a cash-flowing intellectual property asset class.

Why?

Because streaming transformed old songs into recurring annuities.

A hit song from 1999 no longer disappears after radio rotation ends. It lives forever across:

- Spotify

- Apple Music

- YouTube

- TikTok

- movies

- commercials

- sports arenas

- playlists

- nostalgia-driven algorithms

The Chili Peppers reportedly generate around $26 million annually from their catalog alone.

That’s why firms like:

- Sony Music Group

- Universal Music Group

- Warner Music Group

- Bain Capital

are aggressively buying rights portfolios.

This isn’t just about music fandom.

It’s about predictable yield.

The Real Asset Isn’t the Song — It’s the Permanence

What makes a catalog valuable isn’t just popularity.

It’s durability.

The Chili Peppers sit in a rare category of artists whose songs function almost like cultural utility infrastructure:

- gym playlists

- rock radio staples

- sports broadcasts

- algorithmic recommendations

- movie syncs

- guitar-learning staples

- generational discovery

Twenty years after Stadium Arcadium, people are still discovering “Snow (Hey Oh)” for the first time.

That matters financially.

This week, SiriusXM launched a major 20th-anniversary retrospective around Stadium Arcadium, complete with track-by-track commentary from the band.

That’s the flywheel:

- Legacy catalogs create nostalgia

- Nostalgia drives streams

- Streams drive revenue

- Revenue raises catalog valuations

- Valuations attract institutional capital

Music is becoming closer to evergreen software IP than physical media.

Warner Music’s Bigger Bet

One of the most interesting parts of this deal is who bought the catalog.

Warner Music Group has distributed the Chili Peppers since 1991’s Blood Sugar Sex Magik.

So Warner isn’t just acquiring songs.

They’re deepening ownership around an ecosystem they already helped build.

And importantly, Warner reportedly used its joint venture with Bain Capital to fund the purchase.

That tells you something critical about the future:

Private equity increasingly views music catalogs the way previous generations viewed:

- commercial real estate

- pipelines

- telecom infrastructure

- utility assets

The difference?

Songs don’t need maintenance crews.

The Streaming Era Changed the Economics Forever

The CD era created spikes.

Streaming created persistence.

A teenager hearing “Californication” on TikTok in 2026 generates revenue from a song released in 1999.

That’s an extraordinary business model.

And unlike television or film libraries, music consumption is deeply habitual:

- morning playlists

- workouts

- driving

- studying

- restaurants

- sports venues

- retail stores

Music became embedded into daily software behavior.

That makes elite catalogs incredibly resilient.

Catalogs Are the New Media Moat

The bigger story here isn’t just the Chili Peppers.

It’s that catalogs themselves are becoming strategic weapons.

In a fragmented entertainment landscape, ownership matters more than ever.

Who owns:

- the songs,

- the masters,

- the publishing,

- the licensing rights,

- the sync rights,

- the streaming revenue,

- and the cultural memory

will increasingly shape the future economics of media.

The Red Hot Chili Peppers didn’t just sell old songs.

They sold decades of recurring attention.

And in 2026, attention compounds.