The Library of Congress has announced the newest class of recordings entering the 2026 National Recording Registry — a yearly preservation effort designed to protect audio recordings deemed “culturally, historically, or aesthetically significant.”

This year’s list is a fascinating mix of blockbuster pop, country standards, jazz landmarks, dance music pioneers, video game history, Broadway, classic broadcasts, and deeply influential catalog recordings that continue to shape streaming, licensing, sampling, and music culture decades later.

For artists, estates, labels, publishers, and catalog investors, induction into the Registry can reinforce the long-term cultural durability of a recording. These are the kinds of works that continue generating value through:

Streaming

Sync licensing

Sampling

Reissues

Vinyl demand

Film and television placement

Cultural rediscovery cycles

Social media resurgence

Many of these recordings are already deeply embedded into the American cultural bloodstream. Others may receive a renewed spotlight because of the induction itself.

In an era where catalog value increasingly depends on longevity, discoverability, and cross-generational relevance, the National Recording Registry acts almost like an institutional validation of permanence.

The Biggest Takeaways From 2026 National Recording Registry 2026 Class

1. Catalog Longevity Beats Recency

The inclusion of 1989 stands out because it is one of the newest recordings ever inducted.

That’s significant.

The Registry traditionally leans heavily toward older recordings whose historical importance has already stood the test of time. The rapid inclusion of 1989 signals how quickly modern blockbuster pop albums can become culturally foundational.

It also reinforces the staying power of superstar catalogs in the streaming era.

2. Video Game Music Is Now Officially Canon

The induction of the Doom soundtrack is another major moment.

Video game music is no longer niche nostalgia. It is now formally recognized as part of America’s recorded cultural history.

That matters because gaming soundtracks increasingly function like traditional entertainment IP:

Streaming assets

Live performance material

Vinyl collectibles

Licensing opportunities

Fan-community engagement engines

Gaming catalogs are becoming real catalog businesses.

3. Dance Music’s Architects Are Finally Getting Their Due

Frankie Knuckles and Jamie Principle’s Your Love represents a huge acknowledgment of house music’s foundational influence.

Chicago house music helped shape modern EDM, pop production, remix culture, and club music economics globally.

The Registry recognizing dance music history reflects how electronic genres have moved from underground subculture into institutional legitimacy.

4. Sampling History Continues to Matter

The inclusion of Amen, Brother by The Winstons is especially fascinating.

The track contains the famous “Amen Break” — one of the most sampled drum breaks in music history.

That single recording influenced:

Hip-hop

Jungle

Drum and bass

Electronic music

Modern beat production

One drum pattern became a foundational building block for entire genres.

Few examples better demonstrate how catalog value can compound in unpredictable ways over decades.

The Full 2026 National Recording Registry Class 1989 — Taylor Swift Single Ladies (Put a Ring on It) — Beyoncé Weezer (The Blue Album) — Weezer Go Rest High on That Mountain — Vince Gill Doom soundtrack — Bobby Prince The Wheel — Rosanne Cash Rumor Has It — Reba McEntire Your Love — Frankie Knuckles & Jamie Principle I Feel for You — Chaka Khan Texas Flood — Stevie Ray Vaughan and Double Trouble Beauty and the Beat — The Go-Go’s The Devil Went Down to Georgia — The Charlie Daniels Band Chicago Original Cast Album Midnight Train to Georgia — Gladys Knight & the Pips The Fight of the Century broadcast Feliz Navidad — José Feliciano Amen, Brother — The Winstons Turn! Turn! Turn! (To Everything There Is a Season) — The Byrds Modern Sounds in Country and Western Music — Ray Charles The Blues and the Abstract Truth — Oliver Nelson Put Your Head on My Shoulder — Paul Anka Fly Me to the Moon — Kaye Ballard Teardrops from My Eyes — Ruth Brown Mambo No. 5 — Pérez Prado and His Orchestra Cocktails for Two — Spike Jones and His City Slickers

Final Thought

The Registry increasingly reflects a broader definition of what matters culturally.

Rock, pop, jazz, country, hip-hop-adjacent sampling culture, dance music, gaming audio, Broadway, holiday music, and sports broadcasting now all sit under the same preservation umbrella.

That evolution mirrors what’s happening in the catalog business itself.

The modern catalog economy is no longer just about classic rock radio. It’s about multi-format intellectual property that can survive format changes, platform shifts, and generational turnover.

And the recordings that survive longest tend to become the most valuable.

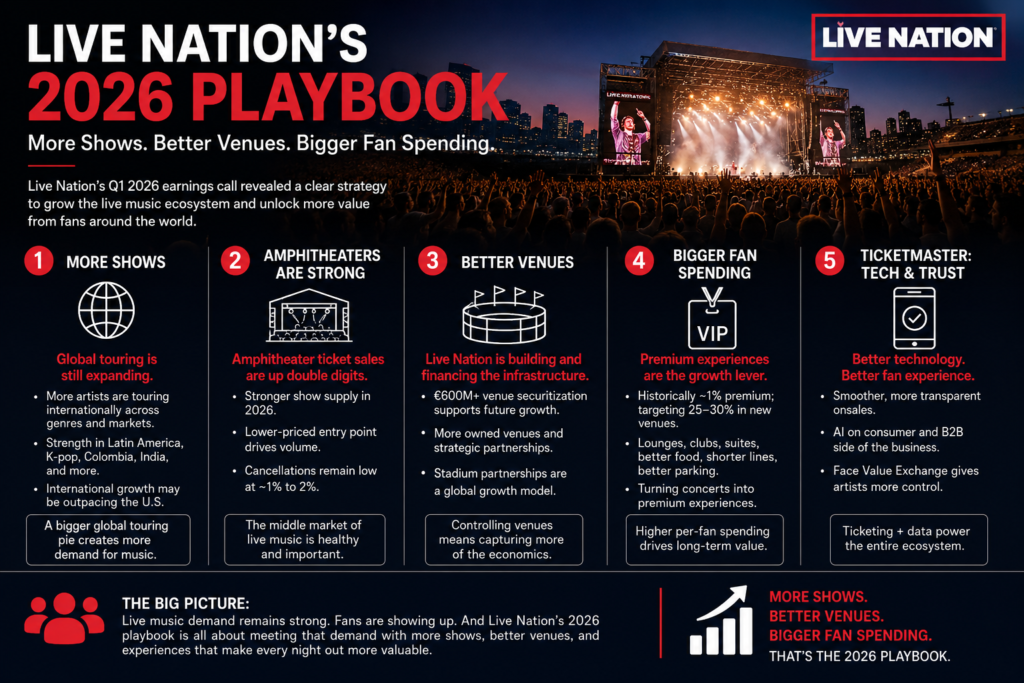

The short version: Live Nation is not just betting on more concerts. It is betting on a bigger live music ecosystem — more global touring, more stadium and amphitheater activity, more owned and partnered venues, better ticketing technology, and higher per-fan spending through premium experiences.

For the music business, that matters. For catalog owners, labels, artists, investors, and anyone watching the economics of music, Live Nation’s call was a reminder that streaming is only one piece of the puzzle. The real money is often built around the fan relationship.

Live music is where that relationship becomes visible.

More Shows: The Global Touring Machine Keeps Expanding

One of the strongest messages from Live Nation management was that global concert supply remains healthy.

CEO Michael Rapino said more artists are touring globally, and that the live music “pie” continues to grow. He pointed to global supply from regions and genres including Latin America, K-pop, Colombia, India, and other international markets. In his view, more artists from more parts of the world are now able to tour across clubs, theaters, arenas, festivals, and stadiums.

That is an important point. Live Nation is not framing growth as dependent on one superstar tour or one geography. The company is talking about a broader, more globalized touring market.

For Catalogs and Cash, this is the key idea: music catalog value becomes more interesting when the audience becomes global.

An artist’s catalog is not just a static bundle of songs collecting streaming royalties. It can become part of a much larger commercial system. Touring can reintroduce fans to older songs. Festivals can expose legacy acts to younger audiences. International markets can create new demand for music that may have already matured in the U.S. or Europe.

The more global the fan base becomes, the more ways there are to monetize the music.

Amphitheaters Are Back in the Story

Live Nation also spent time addressing amphitheaters, which had been a concern in the prior year. Rapino said the company has stronger amphitheater supply in 2026, and that ticket sales are tracking ahead of last year by double digits. He also pushed back on concerns about cancellations, saying the company typically sees a 1% to 2% cancellation rate and that 2026 does not look unusual.

That matters because amphitheaters occupy an important middle lane in the concert business.

Not every artist is a stadium act. Not every catalog is attached to a mega-star. But there is a lot of durable value in artists who can consistently fill amphitheaters, theaters, clubs, and festivals.

Amphitheaters also have a pricing advantage. Rapino described them as a lower-cost entry point compared with arenas and stadiums. That makes them a volume business. For fans who may not want to spend stadium-level money, amphitheaters offer a more accessible live music experience.

This is where the long tail of the music business becomes interesting. Legacy rock acts, country artists, jam bands, alternative bands, nostalgia tours, and multi-act summer packages can all fit into this model.

A catalog does not need to dominate Spotify to have commercial value. Sometimes the better question is: Can this music still move people out of the house?

If the answer is yes, there may be more value there than the streaming chart suggests.

Better Venues: Live Nation Wants More Control of the Infrastructure

The second part of Live Nation’s playbook is venue strategy.

Live Nation is not just promoting shows. It is building, buying, financing, and partnering around venues. CFO Joe Berchtold discussed a venue securitization transaction of just over €600 million, using certain venues as collateral. He described the company’s venue strategy as having something like a property-company/operating-company structure, while still keeping the assets under one roof.

That may sound technical, but the business idea is simple: venues are strategic assets.

If Live Nation controls more of the venue footprint, it can capture more of the economics around the concert. That includes ticketing, sponsorship, food and beverage, premium experiences, parking, hospitality, and long-term fan data.

This is one of the most important ideas in the modern music business: the money is not only in the music itself. It is in the infrastructure around the music.

A song gets the fan interested. The artist gets the fan emotionally committed. The venue turns that attention into a night out. The ticketing platform captures the transaction. The premium experience increases the spend. The sponsor attaches a brand to the moment.

That is the full stack of live music monetization.

Stadium Partnerships Could Become a Global Growth Model

Live Nation also discussed stadium partnerships in Argentina, including arrangements involving Club Atlético and River Plate Stadium. Rapino said the company likes partnering with stadiums globally because many of them are underused compared with NFL-style venues in the U.S.

That is a very interesting model.

Instead of always building from scratch, Live Nation can partner with existing stadiums, bring concerts into the building, add sponsorship expertise, and sometimes provide capital. This can be less capital-intensive than owning or building every venue outright, while still allowing Live Nation to lock up important revenue streams.

For the music industry, this points to a broader trend: live music is becoming more professionalized, more global, and more infrastructure-driven.

For catalog investors, this matters because a stronger live infrastructure can extend the life of music assets. If older artists, reunion tours, tribute events, anniversary shows, and festival appearances become easier to route and monetize globally, then catalogs tied to those artists may have more ways to stay culturally and commercially relevant.

Bigger Fan Spending: Premium Is the Growth Lever

The most interesting part of the call may have been Live Nation’s comments on premium fan experiences.

Rapino said concerts have historically been roughly 99% general admission or standard experience and only 1% premium. But Live Nation sees an opportunity to change that. He said some new arenas could have up to 30% of the house in a premium capacity, while amphitheaters could move from low-single-digit premium levels toward 25% premium.

That is a major shift.

Live Nation wants concerts to look more like sports venues. That means better parking, shorter lines, better food and beverage, hospitality rooms, suites, boxes, lounges, and upgraded experiences.

This makes sense. Fans are not only paying for music. They are paying for the night.

The seat matters. The parking matters. The line matters. The drink matters. The bathroom matters. The ability to avoid chaos matters.

For younger fans, the concert may be a social-media-worthy experience. For older fans, comfort may be the reason they are willing to attend at all. A 50-year-old fan who loves a legacy artist may not want to fight lawn traffic, wait in long lines, or stand all night. But that same fan may pay more for a better experience.

That creates a huge opportunity around legacy catalogs.

Older catalogs often have older fans. Older fans often have more disposable income. If Live Nation can improve the premium experience, it can increase per-fan spending without needing every fan to be a teenager streaming songs all day.

That is a very different way to think about catalog value.

Ticketmaster Is Still Central to the Strategy

Ticketmaster also came up repeatedly on the call.

Rapino said the company is focused on making the onsale process smoother, more transparent, and more confidence-building for fans. He also mentioned using AI on both the consumer side and the B2B side, while building out tools like Face Value Exchange for artists.

Berchtold added that Ticketmaster is using newer approaches, including AI tools, to move faster in markets like Latin America, Asia, and Japan.

The strategic point is clear: ticketing is not just a transaction layer. It is part of the fan relationship.

Who controls the ticketing experience controls a valuable part of the music economy. That company sees demand, pricing, geography, artist strength, fan behavior, and purchase intent.

For artists and catalog owners, this matters because fan data is becoming one of the most important assets in music. A catalog tells you what people listen to. Ticketing tells you what people will leave the house and pay for.

Those are not the same thing.

No Demand Pullback — At Least Not Yet

Live Nation also addressed the big investor question: are consumers pulling back?

Rapino said the company is not seeing a demand slowdown across genres, demographics, geographies, venue types, or price points. He pointed to everything from club shows to amphitheaters to expensive stadium shows and said demand remains strong.

That is a powerful statement, especially in an economy where people keep looking for signs of consumer weakness.

Live music appears to remain a priority. Fans may cut back elsewhere, but the concert is still a major social event. For some fans, it may be one of the few big nights out they plan around all year.

That supports a broader thesis: music remains emotionally durable.

People may change how they consume it. They may shift from CDs to downloads to streaming to short-form video. But the desire to gather around music has not disappeared.

In some ways, it may be stronger because so much of modern life is digital. The live show is physical, social, scarce, and memorable.

That is why it commands pricing power.

The Catalogs and Cash Takeaway

Live Nation’s 2026 playbook is simple:

More shows. Better venues. Bigger fan spending.

But underneath that is a bigger music business lesson.

The value of music is not limited to streaming royalties. Music creates identity, memory, community, and live demand. The companies that can turn that demand into experiences, venues, sponsorships, ticketing, hospitality, and global touring routes are building around the music in ways that can be extremely valuable.

For catalog investors, this should matter.

A catalog is not just a spreadsheet of historical royalties. It is a living asset connected to fan behavior. If the artist can tour, if the music can support a festival slot, if the fan base has spending power, if the songs still create emotional pull, then the catalog may have value beyond passive streaming income.

Live Nation’s call showed that the live music economy still has momentum. The company is investing in venues, expanding globally, improving ticketing, and trying to increase per-fan monetization through premium experiences.

That is not just a concert story.

That is a music asset story.

Bottom Line

Live Nation’s Q1 2026 call was a reminder that the music business is bigger than the stream count.

Streaming tells us what people play. Concerts tell us what people will pay for. Venues show where the money gets captured. Premium experiences show how much more the night can be worth.

And that is the real Catalogs and Cash lesson: the future of music value may belong to the companies that understand not only the song, but the entire economy around the fan.

Warner openly said AI will become a “material contributor” to revenue and profits starting in fiscal 2027. This is no longer theoretical. The company is already using AI for catalog marketing, lyric videos, visualizers, forecasting, reporting, and automation.

2. Catalog Music Is the Economic Engine

Warner said catalog music now represents roughly 65% of recorded music streaming revenue. Older music is becoming more valuable in the streaming era because catalogs can generate recurring revenue for decades.

3. The Labels Want to Monetize AI, Not Just Fight It

Rather than simply resisting AI platforms, Warner is pursuing licensing deals and partnerships. Its relationship with Suno shows the company believes AI music and interactive fan experiences could become major future revenue streams.

4. Modern Record Labels Are Starting to Look Like Tech Companies

The modern label is evolving into an AI-enabled intellectual property platform.

5. Streaming Is Becoming a Higher-Margin Subscription Business

Subscription streaming revenue grew 15%, helped by pricing increases across DSPs. The industry is moving beyond pure user growth and toward higher pricing, premium tiers, and stronger monetization of superfans and interactive experiences.

By 2026, the music catalog business has become something bigger than nostalgia.

It’s infrastructure.

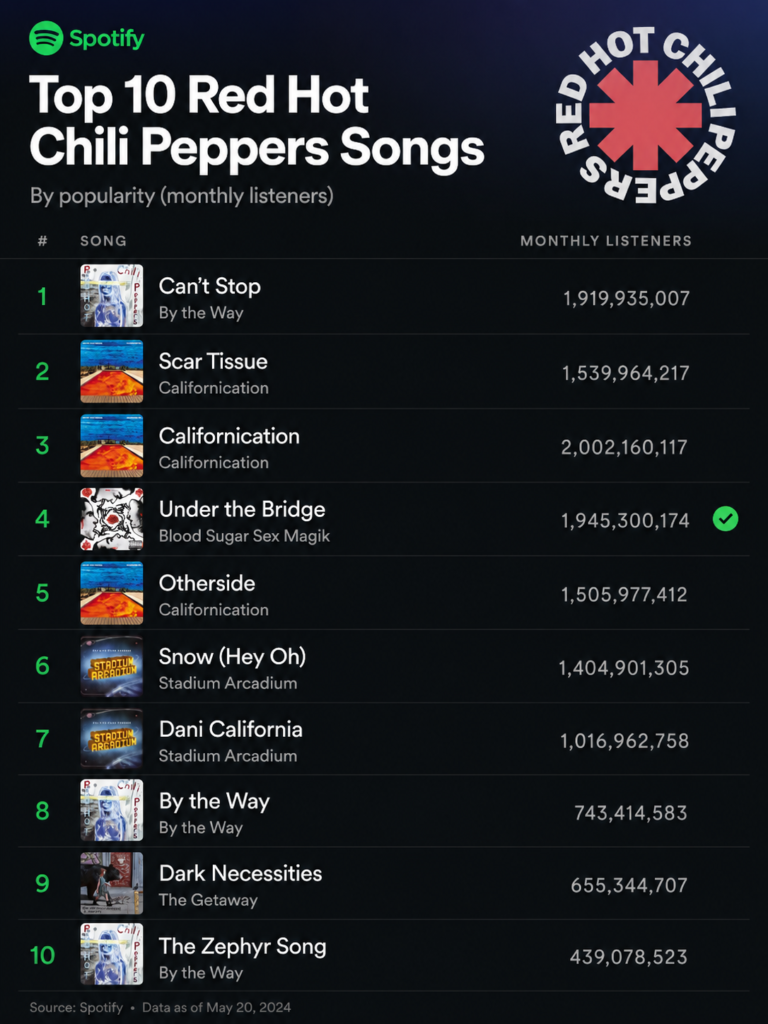

This week, the Red Hot Chili Peppers, with over 46 million monthly listeners on Spotify, reportedly sold their recorded music catalog to Warner Music Group for more than $300 million — one of the largest rock catalog deals in recent memory.

According to Rolling Stone and The Hollywood Reporter, the deal covers the band’s master recordings — the actual sound recordings behind hits like “Californication,” “Under the Bridge,” “Scar Tissue,” “Can’t Stop,” and “Otherside.” They are also the 8th most-played band on SiriusXM Lithium 90’s rock, even though their catalog spans five decades.

And here’s the key detail:

This comes after the band already sold its publishing rights years ago for roughly $140–150 million.

That means the market is now valuing two separate layers of music ownership at enormous scale:

Publishing rights (songwriting/composition)

Master recordings (the recordings themselves)

The Chili Peppers are essentially monetizing decades of cultural relevance twice.

Why Music Catalogs Became Wall Street Assets

Music used to be viewed as entertainment.

Now it’s increasingly viewed as a cash-flowing intellectual property asset class.

Why?

Because streaming transformed old songs into recurring annuities.

A hit song from 1999 no longer disappears after radio rotation ends. It lives forever across:

Spotify

Apple Music

YouTube

TikTok

movies

commercials

sports arenas

playlists

nostalgia-driven algorithms

The Chili Peppers reportedly generate around $26 million annually from their catalog alone.

That’s why firms like:

Sony Music Group

Universal Music Group

Warner Music Group

Bain Capital

are aggressively buying rights portfolios.

This isn’t just about music fandom.

It’s about predictable yield.

The Real Asset Isn’t the Song — It’s the Permanence

What makes a catalog valuable isn’t just popularity.

It’s durability.

The Chili Peppers sit in a rare category of artists whose songs function almost like cultural utility infrastructure:

gym playlists

rock radio staples

sports broadcasts

algorithmic recommendations

movie syncs

guitar-learning staples

generational discovery

Twenty years after Stadium Arcadium, people are still discovering “Snow (Hey Oh)” for the first time.

That matters financially.

This week, SiriusXM launched a major 20th-anniversary retrospective around Stadium Arcadium, complete with track-by-track commentary from the band.

That’s the flywheel:

Legacy catalogs create nostalgia

Nostalgia drives streams

Streams drive revenue

Revenue raises catalog valuations

Valuations attract institutional capital

Music is becoming closer to evergreen software IP than physical media.

Warner Music’s Bigger Bet

One of the most interesting parts of this deal is who bought the catalog.

Warner Music Group has distributed the Chili Peppers since 1991’s Blood Sugar Sex Magik.

So Warner isn’t just acquiring songs.

They’re deepening ownership around an ecosystem they already helped build.

And importantly, Warner reportedly used its joint venture with Bain Capital to fund the purchase.

That tells you something critical about the future:

Private equity increasingly views music catalogs the way previous generations viewed:

commercial real estate

pipelines

telecom infrastructure

utility assets

The difference?

Songs don’t need maintenance crews.

The Streaming Era Changed the Economics Forever

The CD era created spikes.

Streaming created persistence.

A teenager hearing “Californication” on TikTok in 2026 generates revenue from a song released in 1999.

That’s an extraordinary business model.

And unlike television or film libraries, music consumption is deeply habitual:

morning playlists

workouts

driving

studying

restaurants

sports venues

retail stores

Music became embedded into daily software behavior.

That makes elite catalogs incredibly resilient.

Catalogs Are the New Media Moat

The bigger story here isn’t just the Chili Peppers.

It’s that catalogs themselves are becoming strategic weapons.

In a fragmented entertainment landscape, ownership matters more than ever.

Who owns:

the songs,

the masters,

the publishing,

the licensing rights,

the sync rights,

the streaming revenue,

and the cultural memory

will increasingly shape the future economics of media.

The Red Hot Chili Peppers didn’t just sell old songs.

There are moments in the music business where the signal is so obvious, you either see it—or you miss the entire game.

This is one of those moments.

As first reported by Roger Friedman, the “Michael” film is tracking toward $12.5 million in preview revenue—despite functioning less like a traditional biopic and more like a concert experience.

That detail matters.

Because this isn’t a movie story.

It’s a catalog story.

This Isn’t a Film. It’s a Demand Shock.

Audiences aren’t passively watching.

They’re:

Dressing like Michael Jackson

Dancing in theaters

Treating screenings like The Rocky Horror Picture Show-style events

That’s not entertainment.

That’s participation.

And participation is the highest form of catalog engagement.

The Data Just Confirmed It

You don’t have to guess what’s happening.

Amazon’s real-time Top 50 CDs & Vinyl tells the story.

Key Observations from the Current Chart

From your dataset:

Thriller → #2 overall

Off the Wall → Top 15

Bad → Top 20

Number Ones → also charting

At the same time:

Legacy giants dominate:

Abbey Road

The Dark Side of the Moon

Rumours

Legend

And critically:

Greatest hits packages everywhere

The Hidden Pattern: Catalogs Cluster

This is the part most people miss.

When one Michael Jackson album moves…

→ The entire catalog moves.

That’s exactly what we’re seeing:

Thriller pulls attention

Off the Wall captures spillover

Bad benefits downstream

Compilations monetize casual demand

This is not random.

This is catalog clustering behavior.

The Most Important Insight: New Music Is Losing the Battle

Look at the same chart again.

Yes, there are new releases:

Noah Kahan

Olivia Dean

Ringo Starr

But what dominates?

Proven catalogs.

Even more telling:

The “Michael” soundtrack is not leading the charge.

That’s the punchline.

The activation event drives listeners backward, not forward.

Why This Matters for Catalog Investors

If you’re valuing music assets today, this is your model:

1. Activation > Creation

You don’t need new hits.

You need:

Cultural moments

Narrative triggers

Distribution events

2. Emotional Memory Compounds Value

The reason this works:

People don’t consume Michael Jackson as music.

They consume him as:

Memory

Identity

Experience

That’s why accuracy doesn’t matter.

3. Physical Formats Are a Signal, Not a Relic

This Amazon chart is CDs and vinyl.

That matters.

Physical purchases represent:

Intentional demand

Higher-margin fandom

Collector behavior

This is your high-conviction audience.

The Bigger Take: Catalogs Are Experience Engines

The biggest mistake in music investing is thinking you’re buying songs.

You’re not.

You’re buying:

A fan behavior loop

A repeatable activation system

A cultural asset that can be re-triggered

The “Michael” film is just the latest trigger.

Final Take: This Is What $12.5M Really Means

That preview number isn’t about box office.

It’s about elastic demand for elite catalogs.

It proves:

Fans will re-engage regardless of format quality

Legacy hits outperform new releases under pressure

Catalog value is driven by activation—not perfection

And most importantly:

The best catalogs don’t need to evolve. They just need to be turned back on.

Re-recordings have always existed in the music business, but they became impossible to ignore after the success of high-profile artist-driven campaigns that reframed old songs for a new audience. That raises a real question for catalog buyers: do re-recordings hurt the value of masters? The answer is yes, they can, but the impact depends heavily on the artist, the fan relationship, and the nature of the original catalog.

To understand the risk, it helps to remember what a master owner is buying. A master generates value because the original recording continues to be consumed, licensed, and culturally recognized. If an artist creates a new version that listeners adopt as a substitute, some of that value can shift. A catalog buyer may still own the composition-linked economics in some scenarios, but if the transaction centered heavily on the original recordings, substitution risk matters.

That said, not every re-recording meaningfully damages an original master. In many cases, re-recorded versions feel like alternatives rather than replacements. Listeners often remain attached to the original recording because of familiarity, nostalgia, production choices, or the emotional imprint of the first version. A new take may attract attention for a period of time without permanently erasing the commercial power of the original.

The biggest exception is when the artist has a uniquely strong and mobilized relationship with fans. In that case, re-recording becomes more than a musical release. It becomes a loyalty event. Fans are invited to participate in a narrative about ownership, justice, authorship, or artist control. That kind of campaign can create real substitution because fans are not simply choosing a song. They are choosing a side. The commercial effect can be more pronounced because the re-recording carries symbolic meaning.

This is why investors should be careful about overgeneralizing from a few famous examples. A massively engaged global artist with a direct fan-to-artist communication channel is not the norm. Most artists do not have the scale, message discipline, release strategy, and audience behavior required to make re-recordings a dominant substitute for the originals. For many catalogs, the re-recording clause is still a point of risk, but not an existential one.

Another issue is use case. Even if casual listeners continue consuming the old masters, licensing markets may evolve. Supervisors, advertisers, or filmmakers may choose a newer version for practical or narrative reasons. In some situations, they may prefer the re-recording if it is easier to clear, cheaper to license, or more aligned with the artist’s current preferences. That means re-recordings can change not just listening behavior but also commercial pathways.

Catalog buyers therefore need to evaluate several factors. How strong is the artist’s current public connection with fans? How likely is the artist to actively promote replacements? How emotionally attached are listeners to the originals? Are the songs important in sync markets where substitutions can happen more deliberately? Is the catalog so iconic that the original recordings remain definitive no matter what?

There is also a timing element. Sometimes the re-recording risk is highest immediately after release, when press attention and fan mobilization are strongest. Over time, the market may settle into coexistence. Original masters can continue to earn because people return to the familiar recording that first defined the song in culture. In other cases, the new version keeps gaining traction and becomes embedded in playlists and public consciousness.

The takeaway is that re-recordings do introduce real master-value risk, but the severity is context-dependent. Buyers should not dismiss the possibility, especially when dealing with living artists who have both motive and audience leverage. At the same time, they should avoid assuming that every re-recorded catalog becomes impaired in the same way. Music history is full of original recordings that remain the definitive commercial object even when alternatives exist.

So do re-recordings hurt the value of masters? Sometimes, yes. But the deeper truth is that they expose a broader question in catalog investing: are you buying ownership of a recording, or are you buying the enduring listener preference for that recording? In the end, that preference is what determines whether the original master remains powerful.

Not all catalog buyers are solving for the same goal. That is one of the most important truths in the music rights market. Two different bidders can look at the same songs, the same royalty statements, and the same cultural history, then reach very different conclusions about value. The reason is simple: institutional investors and music companies buy catalogs differently because they plan to win in different ways.

An institutional investor usually starts from a financial framework. The question is not simply whether the songs are great. It is whether the cash flows are predictable enough, durable enough, and scalable enough to justify the investment. These buyers think in terms of return targets, hold periods, downside protection, and eventual exit. They want to know what the asset will produce over time and what another buyer might pay for it later. Even if they appreciate the creative side of music, their operating language is still yield, risk, and liquidity.

That means institutional buyers often focus heavily on stability. They like catalogs with proven historical performance, broad consumption, and a lower chance of sudden collapse. They tend to be cautious about overly concentrated catalogs, rights complications, or stories that depend too much on speculative upside. A clean, durable catalog with visible earnings may be more appealing than a glamorous one with a lot of uncertainty.

Music companies come at the asset from a different angle. They are not just buying cash flow; they may also be buying strategic leverage. A music company may have in-house licensing teams, artist relationships, international infrastructure, playlist expertise, marketing muscle, and operational capabilities that allow it to extract more value from the same catalog. Because of that, strategic buyers can sometimes justify paying more. They believe the songs are worth more in their hands than in the hands of a passive owner.

This difference becomes especially clear around upside. An institutional investor may underwrite sync growth conservatively because it does not want the deal to depend on unpredictable events. A music company may look at the same catalog and think, “We have the team to pursue that upside more aggressively.” One buyer sees optionality. The other sees execution leverage. Neither is wrong, but they are framing the opportunity differently.

Time horizon matters too. Institutional buyers often care deeply about how the asset performs within a specific investment window, even if that window has lengthened in recent years. They want to know what happens in three, five, or maybe ten years. Music companies may be more comfortable thinking longer term. They are often built to own rights for decades, not just until the next portfolio event. That longer horizon can make them more tolerant of temporary fluctuations if they believe the catalog has lasting cultural relevance.

The cost of capital also shapes behavior. A large music company may have strategic flexibility that allows it to be more aggressive in competitive auctions. An institutional buyer may face stricter underwriting discipline because its model depends on hitting defined financial thresholds. This can affect pricing, structure, and appetite for complexity. Strategic buyers may accept more operational mess if they think they can fix it. Financial buyers may prefer cleaner assets they can understand quickly and manage efficiently.

There is also a branding dimension. Music companies care about prestige, roster coherence, and long-term positioning within the industry. Owning certain catalogs can strengthen their market identity. Institutional investors may care less about symbolic value and more about portfolio construction. Again, same asset, different objective.

None of this means one class of buyer is smarter than the other. In fact, the music rights market depends on both. Institutional capital helped broaden the market and bring more attention to royalties as an asset class. Strategic buyers bring deep operating knowledge and sector-specific infrastructure. Sometimes they compete. Sometimes they validate each other.

The key point is that catalog valuation is not objective in the purest sense. It is shaped by the buyer’s model of value creation. Institutional investors tend to ask, “What is this worth as a financial asset?” Music companies tend to ask, “What is this worth inside our machine?” Those are related questions, but they are not identical. And when you understand that distinction, the pricing behavior in this market starts to make a lot more sense.

When people talk about music catalog investing, they often focus on the appeal. Recurring royalty income, global consumption, streaming growth, and the emotional durability of familiar songs make catalogs sound almost defensive. But every asset class has its risks, and music rights are no exception. In fact, the biggest mistakes in catalog valuation often come from underestimating the ways a catalog can disappoint after the deal closes.

The first major risk is concentration. A catalog may appear strong because total income looks healthy, but once you open the statements, you may find that one or two songs generate the majority of the revenue. That can be dangerous. If demand for those songs falls, or if usage patterns shift, the valuation can unravel quickly. A broad catalog with many contributors to cash flow is usually safer than a shallow one built on a single classic track.

The second risk is changing consumer taste. Songs do not exist outside culture. Even great songs move through cycles of discovery, nostalgia, overexposure, and rediscovery. A catalog that feels evergreen today may not command the same attention ten years from now. Buyers who assume stable demand forever can get burned. This is especially true for music that was tied heavily to a specific moment, format, or audience. Enduring catalogs tend to have cross-generational recognition or repeated utility in playlists, sync, and cultural memory. The further a catalog is from that kind of durability, the more cautious the underwriting should be.

Rights complexity is another big risk. A song may be commercially attractive but difficult to exploit if the ownership chain is tangled. Multiple writers, samples, disputed shares, approval rights, or inconsistent administration can all reduce value. These issues do not always show up in the headline revenue number, but they affect future monetization. If the catalog is hard to clear for sync licensing or other opportunities, some of the potential upside vanishes in practice.

Platform dependence also matters. If most of a catalog’s earnings are tied to streaming, the buyer is exposed to the economics and algorithms of streaming platforms. That does not automatically make the catalog weak, but it does introduce risk. The business model of music distribution has changed before, and it can change again. A format that feels dominant now may look less central later. The safest catalogs are not necessarily those with the highest streaming numbers, but those with multiple paths to monetization.

Artist reputation creates another layer of uncertainty. A living artist can help increase the value of a catalog through touring, interviews, anniversaries, or renewed cultural relevance. But a living artist can also damage the asset. Public scandals, erratic behavior, or long periods of negative coverage can reduce licensing interest and hurt brand appeal. This is not always catastrophic, and it can be hard to quantify, but it is real. Investors are not only buying songs. They are buying a relationship to the artist’s public story, whether they admit it or not.

Overestimating sync upside is one of the most common valuation mistakes. Buyers love the idea that a song could land in a major film, television show, ad campaign, or viral trailer moment. And yes, that can materially lift earnings. But sync is not an automatic faucet. It is selective, competitive, and often unpredictable. Some catalogs are much better suited to licensing than others. Lyrics, mood, genre, clearance simplicity, and market trends all play a role. If the valuation depends too heavily on “what if this explodes in sync,” the buyer may be paying for a fantasy rather than a cash-flowing asset.

Operational risk matters as well. A catalog is not self-maximizing. Good administration, proactive licensing, metadata accuracy, collection efficiency, and strategic marketing all affect performance. If the buyer lacks the infrastructure to manage the rights well, even a strong catalog can underperform. This is one reason strategic buyers sometimes justify higher prices: they believe they can unlock more value than a pure financial owner can. But that assumption itself is a risk. Synergies sound nice in a deck. Execution is harder.

Market timing is another factor. In frothy periods, buyers can convince themselves that high multiples are justified because the asset class is fashionable. When rates rise, capital tightens, or enthusiasm cools, those same assumptions can suddenly look aggressive. A catalog bought at the peak of optimism may still be a good asset, but that does not mean it was bought at a good price.

The core lesson is simple: music catalogs are attractive, but they are not magic. The biggest risks usually come from concentration, rights friction, taste shifts, platform dependence, reputation issues, overhyped upside, weak operations, and bad timing. Valuation works best when it respects both the numbers and the fragility behind the numbers. Great catalog investors are not just optimistic about songs. They are disciplined about what can go wrong.